Banks have been central to lending for much of history because of their traditional role in accepting deposits from savers and using this capital to make loans to borrowers at higher interest rates. “Alternative lending” simply refers to loans that are originated outside of banks. While non-bank loan channels have always existed in parallel with traditional banking, these were historically small niches in the overall economy.

20 years ago, some savvy entrepreneurs in technology and financial services turned their attention to improving the way that banks provided credit to consumers and small businesses. They discovered the potential for technology to underwrite loans more efficiently and provide borrowers with a better experience—and the alternative lending industry was born. Growth in the space hit an inflection point after the 2008-09 financial crisis, driven by a severe contraction in traditional bank lending and growing mistrust of traditional banks, and accelerated during the COVID-19 pandemic, when consumers moved more financial transactions online.

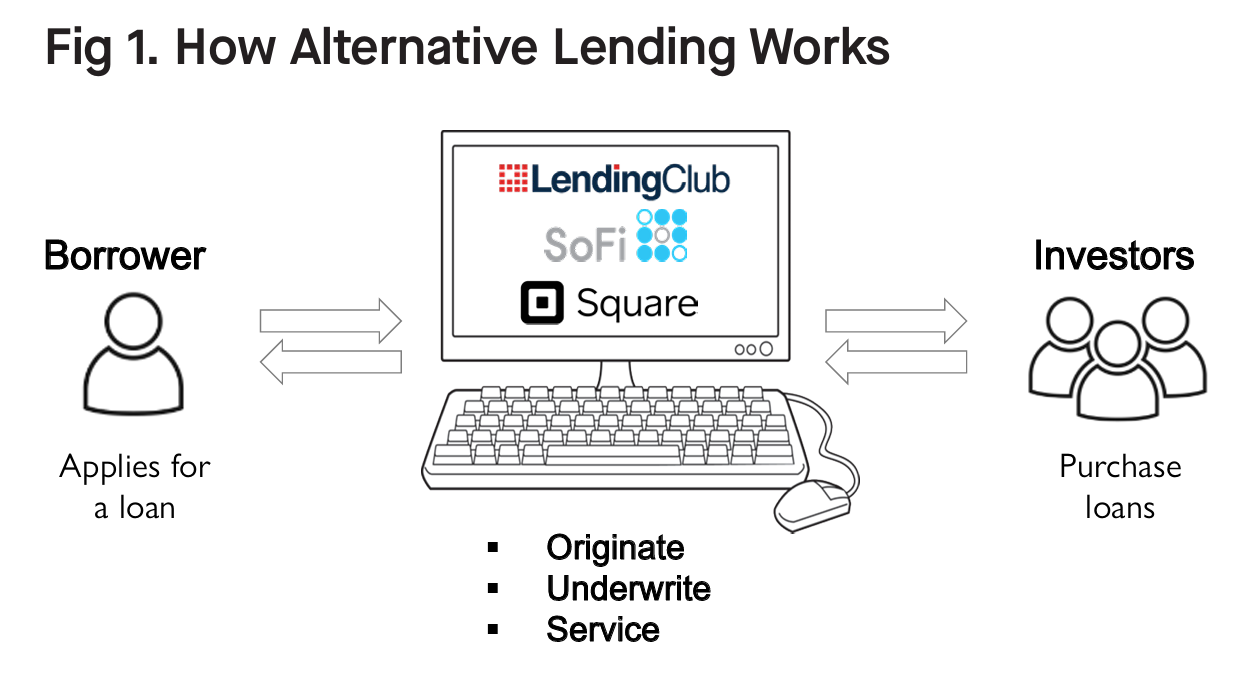

Today, there are several publicly-traded alternative lending companies in the US—you may be familiar with some of the more prominent ones like Lending Club, SoFi, and Square— and collectively, the lending platforms have originated over $250B in loans to date. Despite this scale, there is plenty of room to grow relative to the multi-trillion dollar market for consumer and small business credit currently dominated by traditional banks. Given the benefits for both borrowers and investors, we believe alternative loans have the potential to become a truly mainstream asset class over the next decade.

Alternative Lending Leverages Technology

Alternative lenders perform the same core lending functions that a bank would (Fig. 1): they interface with borrowers to originate the loan; they perform underwriting to gauge a borrower’s credit worthiness and assign a risk based interest rate; and they service the loan, i.e., collect principal and interest on behalf of the lender/investor for the duration of the loan’s life. Instead of funding the loans using deposits, platforms often turn to outside investors to provide the capital.

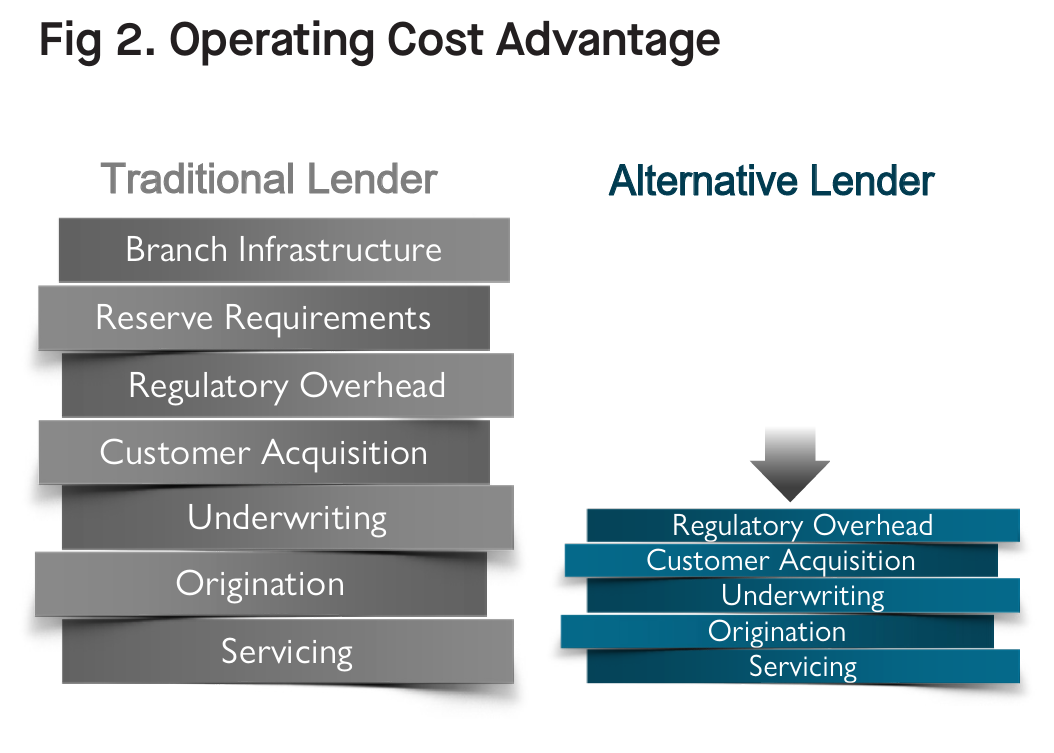

Alternative lenders also differ from banks in their innovative use of technology in the core functions described above. Because most alternative lenders started with a clean slate in the past 10 years, their systems were designed with modern architecture from the ground up. Banks, on the other hand, are notoriously beholden to legacy systems and processes and slow to adopt new technology. They are also saddled with costs from thousands of physical branches.

Alternative lenders have no physical branches, and they rely heavily on technology for tasks like gathering financial documents which can be very labor intensive at banks. We describe this as traditional, “old fashioned” underwriting but using state-of-the-art technology, and it can lead to a significant operating cost advantage relative to traditional banks (Fig. 2). These cost savings can be passed on to borrowers (via lower interest rates) and to investors (via higher yields). Above and beyond the economics, a mostly-online process can provide a better user experience. Many of today’s borrowers prefer not to visit a physical bank branch in order to get a loan.

Loans Designed to be Repaid

Though you may not personally carry a credit card balance, more than 60% of US adults currently do.1 Credit cards have a number of features that can make it difficult for consumers to dig themselves out of debt. Credit cards do not have a set repayment schedule—borrowers are left to choose when to pay back the debt. Credit card interest rates are typically variable and can increase significantly in certain situations, particularly if a borrower misses a payment.

In contrast, alternative loans typically offer borrowers a preset loan size with a fixed interest rate, decided upfront. These loans are amortizing, meaning that borrowers are expected to make regular payments of both principal and interest to repay the loan on a set schedule, typically over 3 to 5 years for consumer loans.

As another example of how the alternative lending industry makes innovative use of technology, monthly payments are usually directdebited from a borrower’s checking account, rather than requiring someone to remember to login to make payments. This is both convenient for borrowers and risk-reducing for investors/ lenders.

A Mainstream Asset Class

Most individual investors have fixed income investments that are limited to corporate bonds and government bonds—that is, lending to big companies and governments. But banks have profitably lent to consumers and small businesses for decades if not centuries. With the growth in alternative lending, many investors are now able to easily invest in consumer credit and small business loans.

The COVID-19 pandemic accelerated the growth of the industry, by driving more consumers and borrowers online. Investors also discovered the resilience of a strategy of lending to prime, creditworthy consumers. The strong loan performance drew a surge of investors into the space, many of whom have come to view alternative loans as a core portfolio allocation. Stone Ridge believes that we are witnessing a fundamental shift in how investors will think about fixed income going forward. By offering higher yields with less interest rate risk, alternative lending can offer a valuable and diversifying contribution to traditional fixed income allocations.